By Ehsanul Hoq

Government securities market of Bangladesh is consist of tradable and non-tradable securities. Non-tradable securities include National Savings Certificates i.e. Sanchayapatras and Sanchayabonds which are only for retail investors.

The tradable securities include Treasury Bills (T-Bills) of 91, 182 and 364 days maturities and Bangladesh Government Treasury Bonds (BGTB) of 2, 5, 10, 15 and 20 years maturities. T-Bills and BGTBs are issued through auctions. Only Primary Dealers (PD) can submit bids in the auctions. Other institutions and individuals can submit bids in auction but through the PDs. At present 20 banks are performing as Primary Dealer. T-Bills and BGTBs can be sold in the secondary market.

Treasury Bills issued by the government as an important tool of raising public finance were of three types, although all of them were 90-day bills. Among these three types, bulk was represented by ad-hoc treasury bills issued to meet the cash balance need of the government. A second type was the 3-months treasury bills on tap introduced in August 1972 and their purpose was to mop up the excess liquidity of banks. The third type was the 3-months treasury bills introduced for subscription exclusively by the non-bank financial institutions, non-financial enterprises and the public.

A market based auction system of treasury bills was introduced from the FY of 2007-08. Under the system, an auction calendar mentioning the date and the amount of price is prepared and made public every year. However, the transaction of the treasury bill of 2 years term has been stopped following the international rules relating to the terms of treasury bills. Moreover the auction of treasury bill having 28 days validity also suspended from 01 July 2008 to avoid overlapping with the 30 day Bangladesh Bank Bill. Following these steps only three categories of treasury bills namely 91-day, 182-day and 364-day bills are now (2012) available in the market for transaction.

The deposit interest rate is paid by financial institutions to deposit account holders. Deposit accounts include certificates of deposit, savings accounts and self-directed deposit retirement accounts. Deposit accounts are attractive places to park cash for investors who want a safe vehicle for maintaining their principle, earning a small amount of fixed interest.

Real Time Analysis

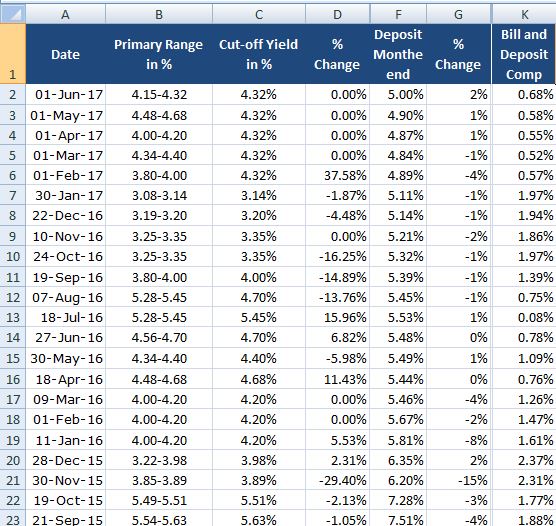

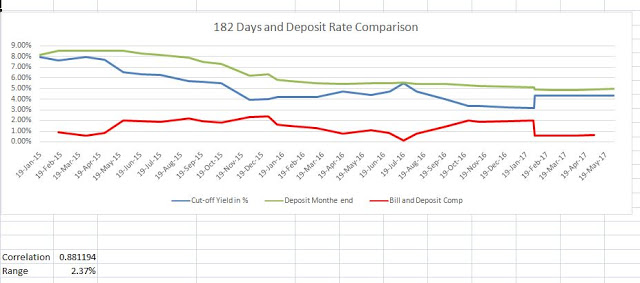

The deposit rate declared by individual banks tend to change less than the Treasury bills which have frequent auctions. So following comparison analysis has been done on 182 day treasury bills and Deposit Rates and the results are shown in a chart.

Results

So the monthly data from September-15 to June-17 has the comparison results. All the deposit rates are weighted average of month end data whereas 182 t-bill data is on the monthly auction rates. We can see that the maximum difference is 2.37% and the minimum is 0.52%. The test statistics show that the range is 2.37% and Correlation is 0.881194 which is good indication that 182 T-bill and Deposit rates in Bangladesh are correlated.

Ehsanul Hoq

Ehsanul Hoq is a research associate and freelance content writer/Blogger